Mergers and Acquisitions (M&A) are pivotal strategies for banks, especially those with large assets, aiming to

enhance their market presence, diversify their portfolio, and achieve economies of scale. In the banking sector,

M&A activities are not just transactions but strategic moves to navigate the competitive landscape, respond to

regulatory changes, and meet evolving customer expectations. For banks with substantial assets, these activities

are critical for maintaining a competitive edge and ensuring long-term sustainability.

The prevalence of M&A in the banking industry underscores its strategic importance. Large banks often engage

in M&A to consolidate their market position, access new technologies, expand into new geographic regions, and

enhance their service offerings. However, overseeing M&A requires meticulous planning, due diligence, and

integration efforts to realize the anticipated benefits and mitigate potential risks.

This article aims to provide a comprehensive guide on overseeing M&A for banks with large assets. It will cover

the strategic rationale behind M&A in the banking sector, outline the steps for successful oversight, and discuss the

challenges and opportunities that come with these complex transactions.

The Strategic Rationale Behind M&A for Large Banks

Seeking Competitive Advantage

M&A offers large banks a pathway to strengthen their market position and outpace competitors. By acquiring or

merging with other banks or financial institutions, large banks can leverage synergies, expand their customer base,

and enhance their product and service offerings, thereby securing a competitive advantage in the market.

Economies of Scale and Scope

Large banks pursue M&A to achieve economies of scale and scope, leading to cost savings and efficiency gains.

M&A allows banks to spread their fixed costs over a larger asset base, optimize their operations, and diversify their

revenue streams. This strategic move not only improves profitability but also enhances the bank's ability to invest in

innovation and technology.

Market Expansion and Consolidation

M&A enables large banks to expand their presence in existing markets or enter new ones, consolidating their position

and increasing their market share. Through strategic acquisitions, banks can access new customer segments, geographic

regions, and niche markets, further solidifying their dominance in the banking sector.

Overseeing M&A Successfully

Due Diligence Process

The due diligence process is a critical component of any successful M&A transaction. For banks with large assets, this

process involves a meticulous examination of the target institution's financial statements, asset quality, loan portfolios,

regulatory compliance records, and operational systems. It also includes an assessment of potential synergies, cultural fit,

and strategic alignment. Banks often involve subject matter experts and legal advisors to ensure thoroughness. The goal

is to identify any material risks or issues that could affect the valuation or post-merger integration of the entities involved.

Integration Planning

Effective integration planning is essential to the success of an M&A deal. Large banks must develop a detailed integration

plan that addresses the consolidation of operations, including people, processes, and technology. This plan should establish

clear communication channels, set timelines, define milestones, and assign responsibilities to integration managers. A

comprehensive technology integration plan is particularly important, as tech integrations can be complex and are often

critical to achieving the deal's objectives.

Risk Management

Managing the risks associated with M&A is a multifaceted task that involves financial modeling, forecasting, and developing

strategies to mitigate identified risks. Large banks must consider the financial implications of the merger, including the impact

on capital ratios, credit risk, and liquidity. They must also plan for operational risks, such as disruptions to customer service and

potential cultural clashes that could affect employee morale and retention. Regular risk assessments and contingency planning

are vital throughout the M&A process.

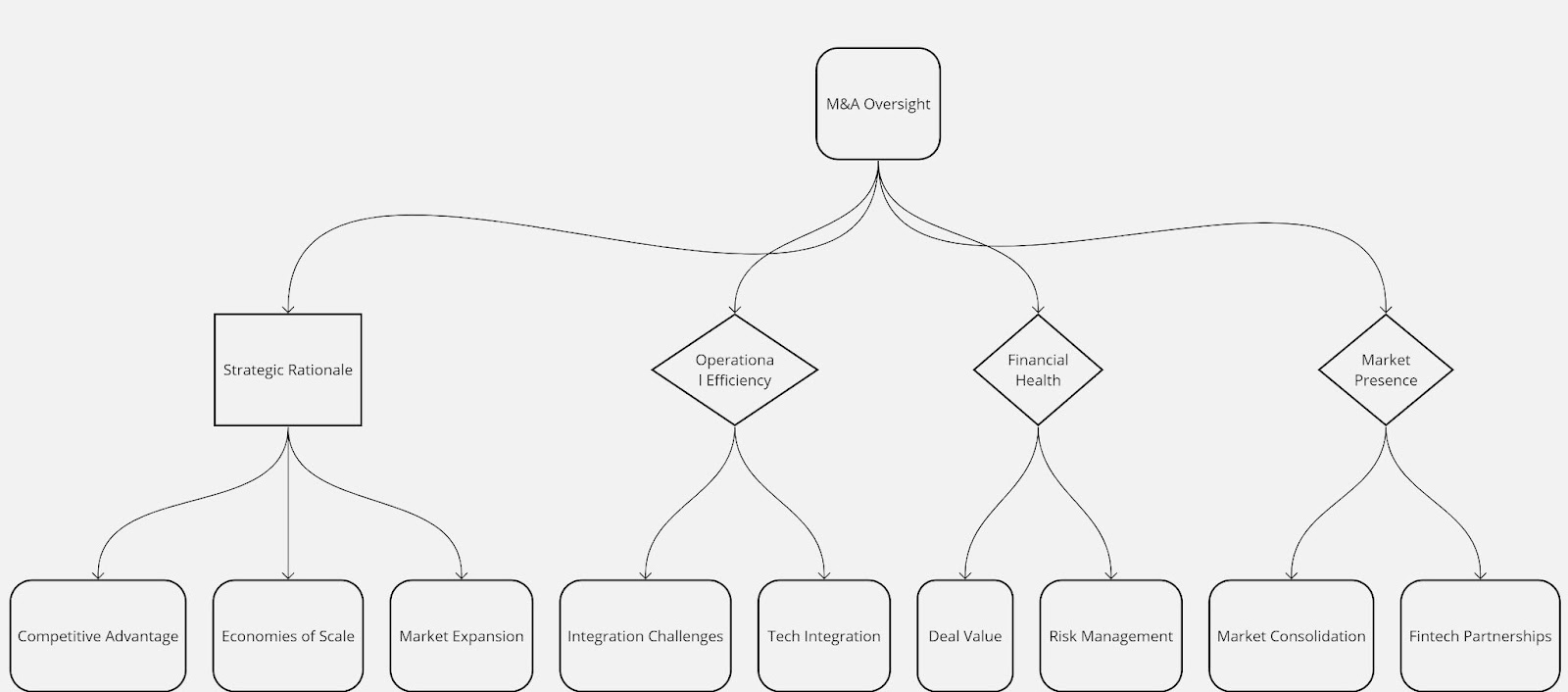

Mastering M&A: A Guide for Large Banks

In the high-stakes world of banking, Mergers and Acquisitions (M&A) stand as crucial strategies for growth, innovation, and

competitiveness. For large banks, overseeing these complex transactions demands a multifaceted approach, focusing on strategic

rationale, operational efficiency, financial health, and enhancing market presence.

Strategic Rationale: At the heart of M&A is the drive for competitive advantage. Large banks leverage M&A to achieve economies

of scale, expand into new markets, and consolidate their positions as industry leaders. These strategic moves enable them to better

meet customer needs, respond to technological advancements, and navigate the regulatory landscape.

Operational Efficiency: The success of M&A hinges on overcoming integration challenges and effectively merging technologies

and cultures. Operational efficiency is paramount, as banks must ensure seamless service delivery, integrate disparate systems, and

harness the power of technology to drive innovation and customer satisfaction.

Financial Health: M&A activities directly impact a bank's financial standing. Managing deal values and risk is critical, with a sharp

focus on maximizing return on investment and ensuring long-term financial stability. This involves diligent risk assessment, strategic

financing, and thorough due diligence to uncover potential synergies and pitfalls.

Market Presence: In the competitive banking sector, M&A serves as a vehicle for market consolidation and forging fintech partnerships.

These strategic alliances not only bolster a bank's market presence but also enable access to cutting-edge technologies and innovative

business models, ensuring the bank remains at the forefront of industry trends.

For banks with large assets, navigating the M&A landscape requires a strategic, informed approach. By focusing on these key areas, banks

can not only ensure the success of their M&A endeavors but also position themselves for sustained growth and leadership in the evolving

banking ecosystem.

Top 5 Challenges in Overseeing M&A for Large Banks

1. Integration Challenges

One of the most significant challenges in M&A is the integration of disparate systems, operations, and cultures. Large banks must manage

the complexities of merging IT infrastructures, harmonizing operational procedures, and blending corporate cultures to create a cohesive

entity. This requires careful planning, significant resources, and a commitment to clear and consistent communication.

2. Regulatory Compliance

Ensuring compliance with a wide array of banking regulations is another challenge in the M&A process. Large banks must navigate federal

and state regulations, as well as international laws if the merger involves cross-border entities. This includes obtaining the necessary regulatory

approvals and ensuring that the combined entity adheres to all compliance requirements.

3. Maintaining Customer Relationships

Maintaining and enhancing customer relationships during and after M&A is crucial for retaining customer trust and loyalty. Large banks must

ensure that customer service remains uninterrupted and that any changes in services or fees are communicated transparently. They must also

address customer concerns promptly to prevent attrition.

4. Managing Financial Risks

Financial risks associated with M&A include the potential for asset devaluation, unexpected costs, and challenges in achieving the forecasted

financial synergies. Large banks must develop accurate financial models and forecasts to manage these risks effectively. Involving financial

analysts and experts can help ensure the reliability of these models.

5. Ensuring Operational Continuity

Ensuring operational continuity during the M&A process is essential to prevent service disruptions that could affect customers and the bank's

reputation. Large banks must establish contingency plans to maintain critical operations throughout the merger, ensuring that all customer-facing

and back-end processes continue to function smoothly.

Overseeing M&A for banks with large assets requires a strategic approach that addresses the complexities of due diligence, integration planning,

and risk management. By understanding and preparing for the challenges associated with M&A, such as integration difficulties, regulatory

compliance, customer relationship management, financial risks, and operational continuity, large banks can enhance their chances of a successful

merger or acquisition. With careful planning, execution, and ongoing management, M&A can be a powerful tool for growth and competitive

advantage in the banking industry.

The Future of M&A in Large Banks

Predicting the Next Wave

The future of M&A in large banks is likely to be influenced by several evolving factors. As the banking industry continues to recover from global

economic uncertainties, M&A is expected to play a crucial role in strategic growth. Large banks may look to M&A to consolidate their positions in

existing markets or to enter new ones, driven by the need to achieve greater scale and efficiency. Additionally, the increasing competition from fintech

firms and non-traditional financial services providers may push large banks to acquire innovative startups to enhance their digital capabilities and meet

changing consumer expectations.

The Role of Technology in M&A

Technology is set to have a profound impact on the M&A landscape. Large banks are increasingly using data analytics and machine learning to identify

potential M&A targets and to perform due diligence more efficiently. During the integration phase, technology plays a critical role in merging IT systems

and digital platforms, which is essential for achieving operational synergies and providing a seamless customer experience. Furthermore, as cybersecurity

becomes a growing concern, banks are also focusing on the technological resilience of their potential M&A partners.

Strategic Alliances vs. M&A

Strategic alliances are becoming an attractive alternative to traditional M&A, especially when banks seek to quickly acquire new capabilities or enter into

new market segments without the complexities of a full merger or acquisition. These alliances, particularly with fintech companies, can provide banks with

access to innovative technologies and business models, enabling them to remain competitive in a rapidly changing financial landscape. However, M&A

remains a key strategy for banks looking to significantly increase their market share or achieve substantial cost savings through economies of scale.

What Are Some Examples Of Successful Strategic Alliances In The Banking Industry

Strategic alliances in the banking industry have been instrumental in fostering growth, innovation, and competitiveness. For instance, Gleason, Mathur, and

Wiggins (2003) examined joint ventures and strategic alliances of financial services firms from 1985 to 1998, highlighting the increasing importance of such

alliances in the complex financial services market.

In the era of digital innovation, banks have formed strategic alliances with fintech companies to adapt swiftly to changing business models and customer needs.

These alliances are often complementary, with banks providing industry knowledge and customer base, and fintechs offering innovative technologies.

A notable example of a successful strategic alliance is the partnership between Webster Bank and NY Jets, which helped distinguish Webster Bank in the market.

Another example is the joint venture between a financial institution and a technology company, where the financial institution provided its knowledge of the

banking industry and its customer base, while the technology company brought in innovative solutions.

Moreover, some banks have used fintechs for innovative application programming or specialized tasks, while others have evolved their business model through

alliances with fintechs. Some fintechs, on the other hand, have pursued alliances with banks primarily to promote their products based on the banks’ trust and

credibility. These examples underscore the strategic value of alliances in the banking industry, enabling banks to leverage external expertise, access new

technologies, and enhance their competitive positioning.

What Are Some Benefits Of Strategic Alliances For Banks

Strategic alliances can offer several benefits for banks. These include:

Strengthened Productivity: Strategic alliances can enhance productivity by combining the strengths and resources of the partnering entities.

Increased Technology-Wide Integrity: Banks can gain access to advanced technologies and platforms through strategic alliances, particularly

with fintech companies. This can help banks improve their services and stay competitive.

Reduced Costs: By sharing resources and expertise, strategic alliances can lead to cost reductions. For instance, a merged bank can reduce

duplication of effort by consolidating operations.

Market Expansion: Strategic alliances can help banks expand their market presence and reach new customer segments.

Risk Management: Strategic alliances can help banks manage risks by spreading the burden of investment and development.

Access to New Skills and Expertise: Each partner in a strategic alliance brings a unique assortment of skills and expertise, which can be

beneficial for banks.

Diversification: Strategic alliances can help banks diversify their offerings and reduce reliance on traditional revenue streams.

Improved Competitive Advantage: Strategic alliances can enhance a bank's competitive position by rationalizing business operations and

integrating innovations.

Exploration of New Opportunities: As the financial services market becomes more complex, strategic alliances become increasingly popular

for firms to explore new opportunities and maintain their competitive advantage.

It's important to note that while strategic alliances can offer numerous benefits, they also come with challenges and risks, such as integration difficulties, regulatory

compliance, and maintaining customer relationships. Therefore, banks need to carefully evaluate potential partners and strategically plan their alliances to maximize

benefits and mitigate risks.

How Do Strategic Alliances Help Banks Expand Their Reach

Strategic alliances help banks expand their reach and enhance their capabilities in several ways:

Access to New Markets and Customer Segments

Strategic alliances enable banks to tap into new markets and customer segments without the need to establish a physical presence or build infrastructure from scratch.

By partnering with local financial institutions or fintech companies, banks can leverage their partners' market knowledge and customer relationships to offer their

services to a broader audience.

Leveraging Complementary Strengths

Banks can form alliances with companies that offer complementary skills and expertise, such as technology firms with advanced digital platforms or non-banking

financial partners with specialized financial services. These partnerships allow banks to enhance their product offerings and provide more comprehensive solutions

to their customers.

Expanding Digital Capabilities

Through strategic alliances with fintech companies, banks can quickly adopt innovative technologies and digital services that appeal to tech-savvy consumers. This

can include mobile banking apps, online payment systems, and personalized financial management tools, which help banks stay competitive in an increasingly digital

world.

Building Reputation and Trust

By forming alliances with reputable partners, banks can enhance their own brand image and build trust with customers. A successful partnership with a well-known

company can signal stability and reliability to customers, which is particularly important in the financial industry.

Achieving Cost Efficiencies

Strategic alliances can lead to cost savings through shared investments in technology, marketing, and product development. By pooling resources, banks and their

partners can achieve economies of scale and reduce the overall cost of entering new markets or developing new products.

Risk Sharing

Entering new markets or launching new products can be risky endeavors. Strategic alliances allow banks to share these risks with their partners, reducing the potential

financial impact on any single entity and providing a safety net for experimentation and innovation.

Enhancing Competitive Position

Strategic alliances are a means of rationalizing business operations and improving the overall competitive position of a bank. By collaborating with other organizations,

banks can strengthen their market presence, fend off competition, and secure a stronger foothold in the industry.

In summary, strategic alliances offer banks a strategic avenue to expand their reach by accessing new markets, leveraging complementary strengths, enhancing digital

capabilities, building reputation, achieving cost efficiencies, sharing risks, and improving their competitive position. These partnerships can be particularly valuable in

today's complex financial services market, where agility and innovation are key to maintaining a competitive edge.

How Do Strategic Alliances Help Banks Gain Access To New Markets

Strategic alliances can help banks expand their reach and gain access to new markets in several ways. Firstly, they can provide banks with the opportunity to leverage

the strengths and resources of their partners, which can be particularly beneficial when entering markets where the partner has an established presence or expertise. This

can help banks overcome barriers to entry and accelerate their market penetration.

Secondly, strategic alliances can enable banks to offer new products and services that complement their existing offerings, thereby attracting new customers and expanding

their market share. For instance, alliances with fintech companies can allow banks to incorporate innovative digital solutions into their service portfolio, enhancing their

appeal to tech-savvy customers and expanding their reach into the digital market.

Thirdly, strategic alliances can facilitate the sharing of knowledge and expertise between partners, which can be instrumental in navigating unfamiliar markets. This can

include insights into local market dynamics, customer preferences, regulatory environments, and more.

Lastly, strategic alliances can enhance a bank's reputation and credibility in new markets, particularly when partnering with well-respected local entities. This can help to

build trust with potential customers and stakeholders, which is crucial for market expansion.

However, it's important to note that the success of strategic alliances in expanding a bank's reach depends on various factors, including the compatibility of the partners, the

alignment of their strategic objectives, the management of the alliance, and the dynamics of the target market.

FAQs on Mergers and Acquisitions in Large Banks

What drives large banks to engage in M&A?

Large banks engage in M&A for various reasons, including the desire to expand their market presence, diversify their product offerings, achieve cost efficiencies, and

respond to competitive pressures. M&A also allows banks to acquire new technologies and talent, which can be critical for adapting to the digital transformation of the

financial services industry.

What are the common challenges faced during the M&A process?

Common challenges during the M&A process include integrating disparate systems and cultures, ensuring regulatory compliance, maintaining customer relationships,

managing financial risks, and achieving the expected synergies. Large banks must navigate these challenges carefully to ensure a successful merger or acquisition.

How can large banks ensure a smooth transition during M&A?

To ensure a smooth transition, large banks should focus on thorough planning, clear communication, and strong leadership. This includes developing a detailed integration

plan, engaging with employees and customers early in the process, and establishing robust governance structures to oversee the transition.

What role does regulation play in banking M&A?

Regulation plays a significant role in banking M&A, as banks must obtain approval from regulatory bodies and ensure that the combined entity complies with all applicable

laws and regulations. Regulatory considerations can influence the structure of the deal, the choice of acquisition targets, and the timing of the transaction.

How does M&A affect the competitive landscape for large banks?

M&A can significantly alter the competitive landscape for large banks by consolidating market power, eliminating competitors, and creating larger entities with increased

resources and capabilities. This can lead to increased competition among the remaining players and may also attract new entrants into the market.

In Conclusion

In overseeing M&A for banks with large assets, it is clear that strategic execution, careful planning, and risk management are key to unlocking value. As the banking industry

faces a mix of challenges and opportunities, M&A remains a competitive differentiator that can lead to faster growth and improved returns. Large banks must approach M&A

with a clear vision, integrating it into their overall corporate strategy and ensuring that they can transition to business-as-usual operations in a seamless and efficient manner.

The future of M&A in large banks will likely be characterized by a careful balance of traditional acquisitions and strategic alliances, with technology playing a central role in

facilitating and integrating these transactions.